|

|

|

|

|

|

Indian finance minister, Yashwant Sinha, feels that he is misunderstood and misjudged for all the right actions he has been taking from North Block, the seat of the Union finance ministry at New Delhi. The Budget for 2000-01, he presented on February 29, is no exception, he says. All the major moves to reform the economy have been ignored by the markets and the intelligentsia. His strategy to take tough measures has been misunderstood and, therefore, criticised. But Sinha is confident that as the true significance of his Budget measures dawns on the markets and the people, he will stand vindicated.

A good reason why Sinha's budget sent shock waves in the stock markets and among the people was the level of expectations the first budget of the new millennium had aroused in them. And Sinha himself was responsible for giving rise to such expectations. Some weeks before he presented the budget, Sinha told a public gathering that the Government's finances were in a mess and he was preparing to bite the bullet on February 29. This was a signal that Sinha would take tough measures in his budget to control the burgeoning gap between the Government's shrinking income and rising expenditure.

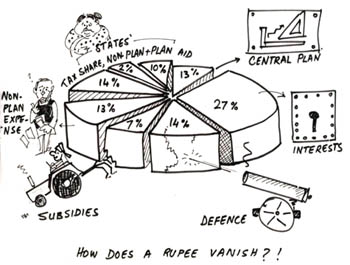

But what happened in the budget was some sort of an anti-climax. He let the Government's total expenditure grow by 11.44 per cent to Rs 3,385 billion (roughly Rs 43.57 is equivalent to one US dollar). What caused greater concern was that his Government's non-plan expenditure (broadly constituting wages and other non-assets creating expenses) went up by a higher margin of 11.89 per cent to Rs 2,504 billion. The outlay on plan expenditure went up by 22 per cent to Rs 1,173 billion, thanks to the compulsions of providing resources for the many schemes and programmes run by the Government.

Sinha also succumbed to pressures from the Defence Ministry to hike defence outlay by 21 per cent to Rs 586 billion. The finance minister justified this in the wake of the India's military clashes with Pakistan recently over Kargil. But a Rs 130 billion hike in defence outlay in a single year was a record and caused a big hole in Sinha's budget.

Additionally, Sinha had no measures in his budget to control his borrowings, which remained at well over Rs 1,000 billion, and his interest payment liability went up by 18 per cent to Rs 1,013 billion. In other words, Sinha's fresh borrowings were not enough to pay up interest charges on past loans - a classic case of India slipping into an internal debt crisis. Additionally, Sinha had no measures in his budget to control his borrowings, which remained at well over Rs 1,000 billion, and his interest payment liability went up by 18 per cent to Rs 1,013 billion. In other words, Sinha's fresh borrowings were not enough to pay up interest charges on past loans - a classic case of India slipping into an internal debt crisis.

No wonder, the Government's fiscal deficit (essentially its gross borrowing requirement) rose to 5.1 per cent of gross domestic product. This may be a little lower than 5.6 per cent fiscal deficit in 1999-00, but nowhere near the level that would let any one in the government breath a little easily. Clearly, biting the bullet was not something that Sinha did in this budget, if the steady expenditure rise and increasing interest payments burden are any indication.

Sinha, of course, defends his position by saying that he had no other option. Expenditure on plan programmes had to increase, while the setting up of the expenditure commission would provide him a set of recommendations for downsizing government and reducing its borrowing requirements. But for all practical purposes, Sinha postponed the task of cutting expenditure to the next budget, or till the recommendations from the expenditure commission are with him, which should take at least a year to be ready.

On the revenue side, however, Sinha showed tremendous courage. He laid a strong foundation for the launch of a single rate central value added tax regime, where every manufacturer within the production chain will pay excise at a unified rate of 16 per cent. For those outside the production chain, the excise duty, rechristened as special excise duty would be paid at three rates. This was path-breaking reform. In addition, Sinha sounded the death knell for the Inspector Raj as far as the excise regime was concerned. On customs side also, he reduced the peak customs rate from 40 per cent to 35 per cent.

He made a bold move for removing the complete income-tax exemption on exporters, by taking way 20 per cent of their concession, and promising that over the next five years, the remaining concessions too would be phased out. The move is astute as the zero tax status for exporters is not compliant with World Trade Organisation norms, and hence had to be phased out. He also doubled the tax on dividend pay-out to 20 per cent and expanded the scope of minimum alternate tax (MAT) applicable to zero-tax companies. There was even an increase in surcharge on personal income-tax for earnings above Rs 150,000 per annum.

The end result of this was that despite fresh taxation by Sinha to the tune of over Rs 69 billion , the fiscal deficit continued to hover at Rs 1,113 billion, about 5.1 per cent of GDP. This was largely because the growth in expenditure was much higher than the projected revenue growth in spite of the new taxes. The markets obviously did not like it. Neither was there any tough measure to cut the government's own expenditure. Nor was the market spared from additional taxes. The only silver linings in the budget were the reform in the excise regime, tax incentives for the venture capital funds, allowing foreign institutional investors a higher ceiling of up to 40 per cent in the stake of Indian companies, a marginal reduction in fertiliser subsidy, better targeting of the public distribution system and a cut in the interest rate for general provident fund deposits. But these were obviously not enough to cheer the market.

The budget for 2000-01 will be remembered not for what measures Sinha initiated, but for the lost opportunities to cut expenditure and introduce fiscal responsibility in governance.

A K BHattacharya is the Managing Editor of Business Standard

|